How to Calculate Your Mortgage Payment: A Complete Guide

I still remember staring at my first mortgage estimate. Numbers everywhere, percentages I didn't understand, and a monthly payment that felt like a gut punch. "Where does all this money go?" I asked myself.

Six years later, having refinanced twice and helped friends navigate their own home purchases, I want to save you that confusion. Here's the real breakdown of what makes up your mortgage payment.

The Four Parts of Every Mortgage Payment

Your monthly payment isn't just "principal and interest" — there are actually four components that lenders bundle together:

- Principal — The actual amount you're borrowing to pay for the home

- Interest — The cost of borrowing money from the lender

- Property Taxes — Set by your local government, usually collected monthly and held in escrow

- Homeowners Insurance — Protects your investment; also typically held in escrow

Some borrowers also have to pay PMI (Private Mortgage Insurance) if their down payment is under 20%, and some have HOA fees that get rolled into the monthly bill.

The Math Behind Your Payment

Let's walk through a real example: a $400,000 home with 20% down ($80,000), leaving a $320,000 loan at 6.5% interest for 30 years.

The formula looks scary, but it's just math:

M = P × [r(1+r)^n] / [(1+r)^n - 1]

Where:

M = Monthly payment

P = Principal ($320,000)

r = Monthly interest rate (6.5% ÷ 12 = 0.005417)

n = Total payments (30 × 12 = 360)Working through it: your monthly payment would be around $2,024 for principal and interest alone. Add property taxes (let's say 1.25% annually = $333/month) and insurance ($150/month), and you're looking at roughly $2,507 total.

That's the number you need to budget for, not just the advertised payment.

Why 20% Down Is the Magic Number

Conventional wisdom says to put down 20%. Here's why it matters:

Below 20%, lenders require PMI. This typically costs 0.3% to 1.5% of your loan amount per year. On that $320,000 loan, that's an extra $96 to $480 per month — money that goes away once you hit 20% equity, but that's often years later.

PMI is basically burning money. You're paying it to protect the lender in case you default, not to protect yourself. The only exception is if you genuinely can't afford a larger down payment without depleting your emergency fund. In that case, the math changes — having cash reserves matters too.

The Interest Rate Trap

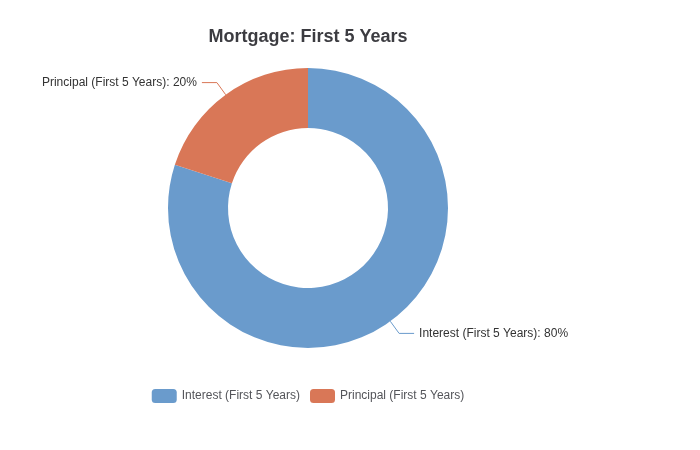

Here's something they don't tell you upfront: in the early years of a 30-year mortgage, most of your payment goes to interest, not principal.

Using our example again, in month one, about $1,733 goes to interest and only $291 reduces your principal. You're paying $6 in interest for every $1 of equity. That's the name of the game.

This is why refinancing or making extra principal payments can save you a fortune over time. Even one extra payment per year shaves about 4 years off a 30-year mortgage and saves tens of thousands in interest.

15 Years vs. 30 Years: The Real Comparison

The 15-year mortgage seems great because you pay less total interest. And you do. But let's look at the actual numbers:

A 30-year loan at 6.5%: $2,024/month, $408,640 total interest over 30 years.

A 15-year loan at 6.0% (yes, rates are typically lower): $2,707/month, $167,230 total interest.

The 15-year saves you $241,000 in interest, but requires $683 more per month. If that payment strain would keep you up at night or prevent you from maxing out retirement accounts, the 30-year with aggressive extra payments might actually be the smarter play. Flexibility has value.

What They Don't Show You on the Estimate

Your loan estimate includes the four components above, but your actual housing cost often includes:

- HOA fees — Can range from $50 to $1,000+ monthly

- Maintenance — Rule of thumb: 1-2% of home value annually ($4,000-$8,000/year on a $400K home)

- Utilities — Often higher than apartments, especially for heating/cooling

- Repairs — Roofs, HVAC, water heaters — they all have lifespans and replacement costs

The "mortgage payment" is just the starting point. Factor in these other costs before you decide how much house you can afford.

Tools to Do the Heavy Lifting

I'm obviously biased, but the mortgage calculator on ToolMixr handles all this automatically. You can model different down payments, compare 15 vs 30-year terms, see the principal/interest split over time, and get a realistic picture before you talk to a lender.

Understanding your mortgage payment isn't about becoming a financial guru. It's about making sure you can actually afford the home you're buying — and sleeping soundly at night knowing where every dollar goes.